First-Time Home Buyer Tax Benefits in Canada: What You Can Claim After Buying Your First Home in 2025

What Tax Credits and Benefits Are Available to First-Time Home Buyers in Canada?

If you purchased your first home in 2025, you may be eligible for several federal tax benefits that can reduce what you owe, or help you recover part of what you spent. These programs are offered through the Canada Revenue Agency and are worth understanding whether you have already filed your return or are preparing to.

This post covers the key programs available to Canadian first-time buyers, what you need to qualify, and what to watch out for before you claim.

The First-Time Home Buyers' Tax Credit (HBTC)

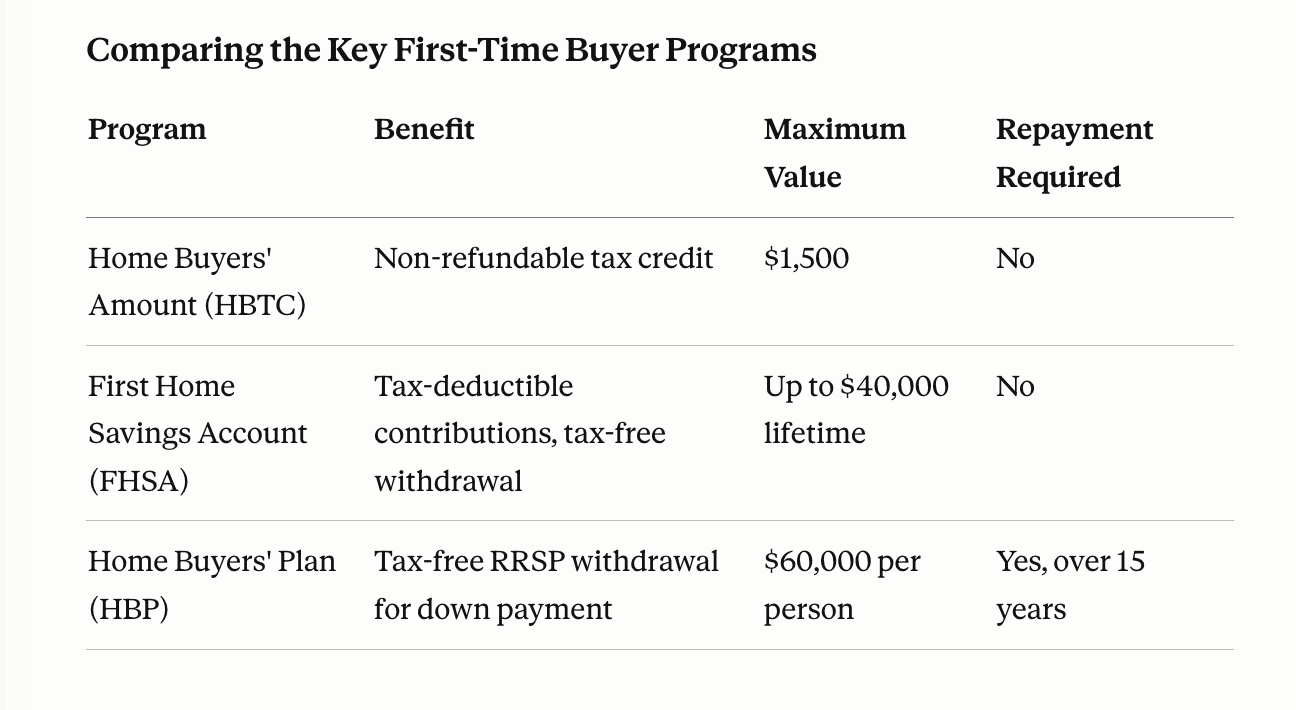

The Home Buyers' Amount is a federal non-refundable tax credit designed to help offset some of the costs of purchasing a qualifying home for the first time.

What it is worth: You can claim up to $10,000 on line 31270 of your federal Schedule 1. This translates to a credit of up to $1,500 against your federal income tax for 2025.

Who qualifies: You (or your spouse or common-law partner) must have purchased a qualifying home in 2025, and neither of you can have owned and lived in another home in that year or in any of the four previous years. This four-year lookback is important - it means some buyers who owned property in the past may now re-qualify if they have been renting since.

What counts as a qualifying home: The property must be located in Canada and registered in your name or your partner's name. It can be a single-family home, semi-detached, townhouse, condominium, or even a home under construction, as long as you move in within one year of purchase.

Splitting the credit: If you purchased jointly with a spouse or common-law partner, you can split the $10,000 claim in any proportion you choose. However, the combined total cannot exceed $10,000. A practical note: because this is a non-refundable credit, it is most effective when claimed by the person who has at least $1,500 in federal tax owing. If your tax bill is lower than that, the unused portion of the credit cannot generate a refund.

How to claim it: Enter up to $10,000 on line 31270 of your federal return. No supporting documents need to be filed, but keep your purchase agreement, title documents, and related paperwork in case CRA requests them later.

The First Home Savings Account (FHSA)

If you purchased in 2025 using funds from a First Home Savings Account, you likely already benefited from one of the most powerful savings tools available to Canadian first-time buyers.

The FHSA allows eligible individuals to contribute up to $8,000 per year, up to a lifetime maximum of $40,000. Contributions are tax-deductible - similar to an RRSP - and qualifying withdrawals for a home purchase are entirely tax-free, similar to a TFSA. The combination makes it uniquely effective for building a down payment.

If you contributed to an FHSA in 2025 and have not yet claimed the deduction, that deduction can be carried forward and applied in a future tax year when it may provide greater benefit.

The Home Buyers' Plan (HBP)

The Home Buyers' Plan allows first-time buyers to withdraw up to $60,000 from their RRSP on a tax-free basis to use toward the purchase of a qualifying home. Withdrawals made under the HBP must be repaid to the RRSP over a 15-year period, with repayment beginning no later than the second year following the year of withdrawal (for withdrawals made before January 1, 2022) or the fifth year following the withdrawal (for withdrawals made between January 1, 2022 and December 31, 2025, under the extended grace period).

The HBP and FHSA can both be used toward the same home purchase, which is a significant advantage for buyers who have been saving in both accounts.

Common Questions First-Time Buyers Ask

I owned a condo five years ago. Do I still qualify as a first-time buyer? Possibly, yes. The four-year rule looks back from the year of purchase. If you did not own and live in a qualifying home in 2025 or in any of 2024, 2023, 2022, or 2021, you likely qualify - depending on the specific timing of your previous ownership.

Can my partner and I each claim the full $10,000? No. The maximum combined claim for any one home is $10,000. You can split it in any proportion, but the total cannot exceed that amount.

What if I owe less than $1,500 in federal tax? The HBTC is non-refundable, which means it can only reduce your taxes to zero. Any unused portion of the credit is not returned to you as a refund.

Does the home have to be my primary residence? Yes. The home must become your principal place of residence within one year of purchase.

I bought with a friend, not a spouse. Can we each claim part of the credit? Yes. When multiple eligible individuals purchase the same home, they can each claim a portion of the credit, as long as the combined total does not exceed $10,000.

Practical Checklist for First-Time Buyers Filing in 2026

- Confirm you did not own and live in a home in 2021, 2022, 2023, 2024, or 2025 (before your purchase)

- Verify the home is registered in your name or your partner's name

Confirm the home became (or will become) your principal residence within one year - Claim up to $10,000 on line 31270 of your Schedule 1 federal return

- If filing jointly, decide how to split the claim based on each partner's tax liability

- Keep your purchase agreement and title documents in a secure location

- If you used an FHSA or HBP, confirm those withdrawals were properly documented and reported

- Consult a tax professional if you have questions about eligibility, particularly if you had previous homeownership

A Note on the GST/HST New Housing Rebate

If you purchased a newly built home or substantially renovated property, you may also be eligible for the GST/HST New Housing Rebate, which allows you to recover a portion of the federal tax paid on the purchase.

Separately, the new First-Time Home Buyers' GST/HST Rebate - introduced for purchase agreements signed on or after March 20, 2025 - eliminates the GST (or the federal part of the HST) entirely on new homes valued up to $1 million for eligible first-time buyers. These programs are distinct from the HBTC and worth discussing with your accountant or builder.

Final Thought

The programs covered here are among the most straightforward financial benefits available to Canadian first-time buyers. The Home Buyers' Amount in particular takes minutes to claim and requires no additional documentation at filing. If you purchased in 2025 and have not already looked into these programs, this tax season is the right time to do it.

If you are planning to purchase your first home and want to understand how all of these programs fit into your broader mortgage and financial strategy, I am happy to talk it through with you.

Book a call at www.MortgageCall.ca or email [email protected]